In the last three decades, most large cities in the world have experienced strong inflation of real estate prices. This overall increase - to a varying degree - is a source of major imbalances. The link between residential densification, privatisation of housing markets and unaffordability is strengthening. There is a risk of making these cities unaffordable and unliveable even for the middle-class. Urban liveability strategies are emerging as a response to this situation, and becoming an factor of competitiveness.

All over the world, housing costs are becoming increasingly disconnected from incomes in large cities. This is a major phenomenon in both scale and duration. International comparisons of housing costs are not easy to make, especially on the scale of major metropolitan areas. These are generally based on indexes determined and calculated on a national scale. Despite varying situations in each country’s real estate markets, data shows a very strong and convergent global increase in property prices since the 1990s. Using price data compiled for 42 EU and OECD member states, economist Jean Cavailhès1 has shown that 16 countries saw real estate prices more than double between 1996 and 2007 (including France, the UK and Spain), while 12 others saw increases of between 50 and 100% (including the USA). Only 5 countries (including Germany) saw property prices fall over the same period. As Cavailhès states, “This international convergent increase is unique in history. Moreover price rises have never been so high, and the upward trend has never lasted so long”. In Europe, although prices fell slightly following the subprimes crisis in 2007-2008, they began to rise again in 2013. Prices have even risen sharply in Germany since 2010.

Real estate inflation in world cities

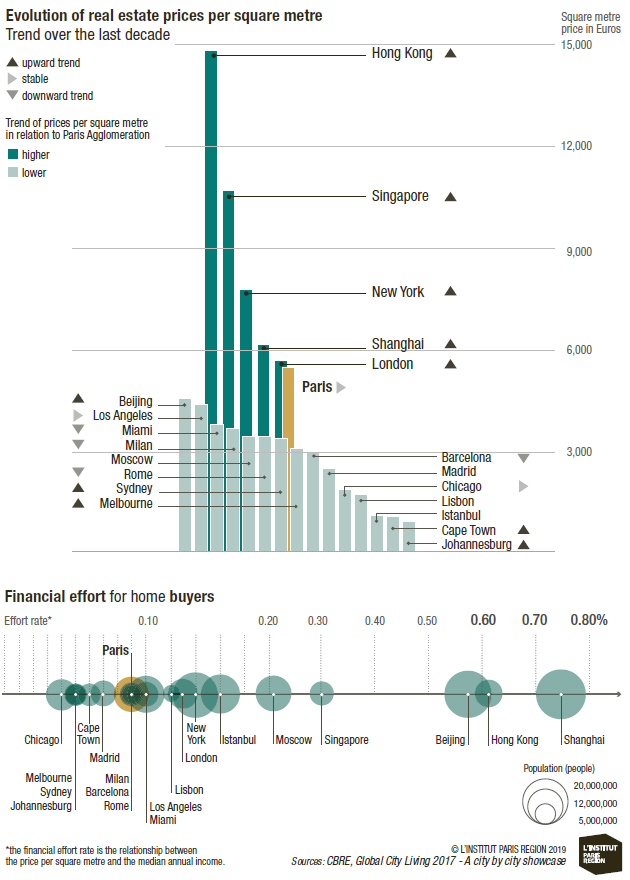

In the light of this nationwide data, it comes as no surprise that world cities, which are generally characterised by extremely tight property markets in their respective countries, have seen even sharper rises in property prices. The Paris Region (Île-de-France) has seen real estate prices more than treble since the mid 1990s. According to the latest available CBRE data, Hong Kong is currently by far the most expensive city in the world for real estate, with prices per square metre nudging 15,000 euros (and up to 29,000 € in prime areas), followed by Singapore, New York, Shanghai and London. According to CBRE, Paris (agglomeration) comes in at 6th place with prices slightly above 5,400 euros per square metre; and only at 10th place if we only consider prime areas, which, at less than 15,000 € per square metre, lag behind cities such as Sydney, Moscow and even Lisbon. The low score of Paris can partly be explained by the weakness of the euro against the dollar when the survey was carried out. This data also confirms that, in many world cities, the post-subprime period also corresponded to a sharp rise in real estate prices, sometimes with two-figure annual growth rates, as in Shanghai, Beijing, Hong Kong and Toronto. This also concerns cities famed until now for their “liveability”, such as the largest Australian and Canadian cities, as well as Berlin, which does not appear in the CBRE data. Local attractiveness strategies largely based on the liveability of a city and the relative affordability of its housing can thus, when successful, result in real estate inflation and thus erode this initial affordability. In a way this phenomenon of “top-down” market standardisation reproduces, on a national or even international scale, the gentrification observed in large cities.

Metropolitan "housing crisis" on a global scale?

Real estate inflation in large cities has restricted access to real estate markets for the less affluent. Many of these cities are experiencing a real housing crisis. By allowing us to compare real estate prices to average income in different cities2, the data made available by CBRE suggests that there are contrasting situations from one city to the next. There is no simple relationship between the effort required to purchase a home and the population of each city: Although larger cities tend to induce stronger economic attractiveness and increased competition for premium space, in certain cities real estate prices still adapt to income levels that are on average higher than in the rest of the country. This means that the financial effort required (with respect to income) turns out to be comparable, or even lower, in cities such as Paris, London or Los Angeles, than in smaller European cities such as Lisbon, Rome, Barcelona or Madrid. But price per square metre can also conceal choices that have to be made regarding the size of the units purchased, which of course significantly impacts “liveability” for households. Even though the CBRE data requires a degree of circumspection, it does tend to show, for example, that Paris stands apart for the particularly small size of its housing units (about 60 square metres on average), which is smaller than homes sold in London (96 sq.m.) and even smaller compared to cities where property development tends to favour single-family houses rather than apartments (124 sq.m. in Los Angeles and 151 sq.m. in Sydney). We see a much more significant mismatch between real estate prices and average income in countries whose economic development is more recent, in particular some of the largest cities in Asia. Singapore and Chinese cities (Beijing, Shanghai and Hong Kong) clearly stand apart from the model of other cities covered in the CBRE survey regarding affordability. These high-density cities are characterised by significant income inequalities, a fact that biases data that only looks at real estate prices and thus home ownership.

Liveability and affordability, key issues for metropolitan Paris

Compared to these extreme examples, the liveability of European cities, such as Paris with its agglomeration, can be seen as a model to be preserved as they face continuous population growth and rising housing prices. More and more world city benchmarks3 include indicators of liveability and housing affordability for employees. Ranked 39th (just ahead of Lyon and London) in the 2018 edition of Mercer’s Quality of Living Ranking, Paris remains “well ranked for its size”, despite rising living costs, given that “the highest-ranked cities are generally medium- sized”. The financial effort for housing within the agglomeration of Paris remains, on average, relatively low in comparison with other world cities of comparable or smaller size. Paris is characterised by the relatively small gap between prices per square metre in prime areas and the rest of the agglomeration, the former being on average only 2.1 times higher than the latter. In the least balanced metropolitan markets, this multiplicand can be significantly higher: 7 in Lisbon, 6.9 in Sydney, 4.3 in London, and 3.9 in Moscow. But what is true of international cities is not necessarily to be applied on a national scale. Prices in the Paris Region, for example, remain significantly higher than in other French cities. And for its households that are not in the upper income brackets, especially families with children, the residential attractiveness of smaller cities can be greater, provided they offer suitable employment opportunities, or when new working practices (teleworking, third places, etc.) combined with efficient transport solutions, make it possible to travel rapidly to the economic centre of Paris. Given these new opportunities for weighing up economic and residential attractiveness, as well as their implications on the urban models and on commuting, metropolitan housing strategies are inevitably at a crossroads. The sustainability of the current model of development of the largest cities, less and less inclusive for the poor, needs to be questioned. Combined with the increasing environmental issues, could this ultimately limit the attractiveness and economic dynamism of literally “unliveable” metropolitan areas?

Emmanuel Trouillard, Housing Planning Officer, L’Institut Paris Region

1. Les prix des logements et leurs déterminants fondamentaux. Analyse des évolutions internationales en longue période, May 2018. Website: politiquedulogement.com.

2. A rough indicator of the fi nancial effort required from prospective home owners.

3. Publications designed by consultancy firms, mainly in the service of multinational enterprises.

4. Emmanuel Trouillard (coord.), Métropolisation et Habitat, IAU-IdF’s contribution to the diagnosis of the PMHH (Metropolitan Housing and Accommodation Plan) of the Métropole du Grand Paris, Sept. 2018.

GLOBAL CITY LIVING REPORT

The Global City Living Report. A City by City Guide 2017 published by the real estate consulting fi rm CBRE, which provides property and rental prices for 29 world cities (both entire cities and prime areas: the most sought-after areas, seen as the safest investment opportunities). This data must be handled with care: in addition to the usual problems relating to the size of the area covered (which can vary quite a lot from city to city) and the uniformity of available data from one country to another, average disposable income fi gures fail to take into account not only differences in taxation and social contributions, but also the distribution of the income across the total population. Such comparisons thus have their limits. The structure of local property markets (proportion of home owners, proportion of non-market self-builds, etc.) should ideally also be taken into account.